Familiarity with the basic concepts and techniques from probability theory and

mathematical statistics can best be gained by studying suitable textbooks and

exercising those concepts and techniques by solving instructive problems.

The books by DeGroot and Schervish [2011], Hoel et al. [1971a], Hoel

et al. [1971b], Feller [1968], Lindley [1965a], and Lindley [1965b] are highly

recommended for this purpose and appropriate for readers who will have studied

mathematical calculus in university courses for science and engineering

majors.

This document aims to provide an overview of some of these concepts and

techniques that have proven useful in applications to the characterization,

propagation, and interpretation of measurement uncertainty as described, for

example, by Morgan and Henrion [1992] and Taylor and Kuyatt [1994], and in

guidance documents produced by international organizations, including the Guideto the expression of uncertainty in measurement (GUM) [Joint Committee for

Guides in Metrology, 2008a] and its supplements [Joint Committee for Guides in

Metrology, 2008b]. However, the examples do not all necessarily show a direct

connection to measurement science.

Our basic premises are that probability is best suited to express uncertainty

quantitatively, and that Bayesian statistical methods afford the best means to

exploit information about quantities of interest that originates from multiple

sources, including empirical data gathered for the purpose, and preexisting expert

knowledge.

Although there is nothing particularly controversial about the calculus of

probability or about the mathematical methods of statistics, both the meaning of

probability and the interpretation of the products of statistical inference continue

to be subjects of debate.

This debate is meta-probabilistic and meta-statistical, in the same sense as

metaphysics employs methods different from the methods of physics to study the

world. In fact, the debate is liveliest and most scholarly among professional

philosophers [Fitelson, 2007]. However, probabilists and statisticians often

participate in it when they take off their professional hats and become

philosophers [Neyman, 1977], as any inquisitive person is wont to do, at one time

or another.

For this reason, we begin with an overview of some of the meanings that

have been assigned to probability (§2) before turning to the calculus of

probability (§3). In applications, the devices of this calculus are typically

brought into play when considering random variables and probability

distributions (§4), in particular to characterize the probability distribution of

functions of random variables (§5). Statistical inference (§6) uses all of

these devices to produce probabilistic statements about unknown quantity

values.

2 Probability

2.1 Meaning

In Truth and Probability [Ramsey, 1926, 1931], Frank Ramsey takes the

view that probability is “a branch of logic, the logic of partial belief and

inconclusive argument”. In this vein, and more generally, probabilities

serve to quantify uncertainty. For example, when one states that, with

confidence, the distance between two geodesic marks is within 0.07 m

of 936.84 m, one believes that the actual distance most likely lies

between 936.77 m and 936.91 m, but still entertains the possibility that

it may lie elsewhere. Similarly, a weather service announcement of

chance of rain tomorrow for a particular region summarizes an assessment of

uncertainty about what will come to pass.

Although relevant to the interpretation of measurement uncertainty, and generally

to all applications of probability and statistics, the meaning of probability

really is a philosophical issue [Gillies, 2000, Hájek, 2007, Mellor, 2005].

And while there is much disagreement about what probabilities mean,

and how they are created to begin with (interpretation and elicitation of

probability), there also is essentially universal agreement about how numerical

assessments of probability should be manipulated and combined (calculus of

probability).

2.2 Chance and Propensity

Chances arise in connection with games of chance, and with phenomena that

conceivably can recur under essentially the same circumstances. Thus one speaks

of the chances of a pair of Kings in a poker hand, or of the chances that the

nucleus of an atom of a particular uranium isotope will emit an alpha particle

within a given time interval, or of the chances that a person born in France will

have blood of type AB. Chances seem to be intrinsic properties of objects

or processes in specific environments, maybe propensities for something

to happen: their most renowned theorists have been Hans Reichenbach

[Reichenbach, 1949], Richard von Mises [von Mises, 1981], and Karl Popper

[Popper, 1959].

2.3 Credence and Belief

Credences measure subjective beliefs. They are best illustrated in relation with

betting on the outcomes of events one is uncertain about. For example, in this

most memorable of bets offered when the thoroughbred Eclipse was about to run

against Gower, Tryal, Plume, and Chance in the second heat of the races on May

3rd, 1769, at Epsom Downs: “Eclipse first, the rest nowhere”, with odds of 6-to-4

[Clee, 2007].

The strength or degree of these beliefs can be assessed numerically by techniques

that include the observation of betting behavior (actual or virtual), and this

assessment can be gauged, and improved, by application of scoring rules

[Lindley, 1985].

Dennis Lindley [Lindley, 1985] suggests that degrees of belief can be measured by

comparison with a standard, similarly to how length or mass are measured. In

general, subjective probabilities can be revealed by judicious application of

elicitation methods [Garthwaite et al., 2005].

Consider an urn that contains 100 balls that are identical but for their colors:

are black and

are white.

The urn’s contents are thoroughly mixed, and the standard is the probability of the event

of drawing a black ball.

Now, given an event ,

for example that, somewhere in London, it will rain tomorrow,

whose probability he wishes to gauge, Peter will select a value for

such that he regards

gambling on as

equivalent to gambling on

(for the same prize): in these circumstances,

is Peter’s

credence on .

The beliefs that credences measure are subjective and personal, hence the

probabilities that gauge them purport to a relationship between a particular

knowing subject and the object of this subject’s interest. These beliefs certainly

are informed by such knowledge as one may have about a situation, but they also

are tempered by one’s preferences or tastes, and do not require that a link be

drawn explicitly between that knowledge or sentiment and the corresponding bet.

Bruno de Finetti [de Finetti, 1937, 1990], Jimmie Savage [Savage, 1972], and

Dennis Lindley [Lindley, 2006] have been leading developers of the subjective,

personalistic viewpoint.

2.4 Epistemic Probability

Logical (or epistemic, that is, involving or relating to knowledge) probabilities measure

the degree to which the truth of a proposition justifies, warrants, or rationally

supports the truth of another [Carnap, 1962]. For example, when a medical doctor

concludes that a positive result in a tuberculin sensitivity test indicates tuberculosis

with

probability (§3.6), or when measurements made during a total eclipse of the sun

overwhelmingly favor Einstein’s theory of gravitation over Newton’s [Dyson

et al., 1920].

The fact that scientists or judges may not necessarily or explicitly use

probabilities to convey their confidence in theories or in arguments

[Glymour, 1980] does not reduce the value that probabilities have in

models for the rational process of learning from experience, either for

human subjects or for reasoning machines that are programmed to make

decisions in situations of uncertainty. In this fashion, probability is an

extension of deductive logic, and measures degree of confirmation: it does

this objectively because it does not involve subjective personal opinion,

hence is as incontrovertible as deduction by any of the forms of classical

logic.

The difficulty lies in specifying a starting point, a state of a priori ignorance that

is similarly objective and hence universally acceptable. Harold Jeffreys

[Jeffreys, 1961] provided maybe the first modern, thorough account of how this

may be done. He argued, and illustrated in many substantive examples, that it is

fit to address the widest range of scientific problems where one wishes to exploit

the information in observational data.

The interpretation of probability as an extension of logic makes it particularly

well-suited to applications in measurement science, where it is desirable

to be able to treat different uncertainty components, which may have

been evaluated using different methods, simultaneously, using a uniform

vocabulary, and a single set of technical tools. This concept underlies the

treatment of measurement uncertainty in the GUM and in its supplements.

Richard Cox [Cox, 1946, 1961] and Edwin Jaynes [Jaynes, 1958, 2003] have

articulated cogent arguments in support of this view, and José Bernardo

[Bernardo, 1979] and James Berger [Berger, 2006] have greatly expanded

it.

2.5 Difficulties

Even in situations where, on first inspection, chances seem applicable, closer

inspection reveals that something else really is needed.

There may be no obvious reason to doubt that the chance is ½ that a coin tossed

to assign sides before a football game will land Heads up. However, if the coin

instead is spun on its edge on a table, that chance will be closer to either

or

than

to ½ [Diaconis and Ylvisaker, 1985].

And when it is the magician Persi Warren [DeGroot, 1986] who tosses the coin,

then all bets are off because he can manage to toss it so that it always lands

Heads up on his hand after he flips it in the air: while the unwary may be

willing to bet at even odds on the outcome, for Persi the probability is

1.

And there are situations that naturally lend themselves to, or that even seem to

require, multiple interpretations. Take the 20 % chance of rain: does this mean

that, of all days when the weather conditions have been similar to today’s in the

region the forecast purports to, it has rained some time during the following day

with historical frequency of 20 %? Or is this the result of a probabilistic forecast

that is to be interpreted epistemically? Maybe it means something else altogether,

like: of all things that will fall from the sky tomorrow, 1 in 5 will be a

raindrop.

2.6 Role of Context

The use of probability as an extension of logic ensures that different people who

have the same information (empirical or other) about a measurand should

produce the same inferences about it. Example §2.7 illustrates the fact that

contextual information relating to a proposition, situation, or event, will influence

probabilistic assessments to the extent that different people with different

information may, while all acting rationally, produce different uncertainty

assessments, and hence different probabilities, for the same proposition, situation,

or event.

When probabilities express subjective beliefs, or when they express states of

incomplete or imperfect knowledge, different people typically will assign different

probabilities to the same statements or events. If they have to reach a

consensus on a course of action that is informed by their plural, varied

assessments, then they have to engage in a harmonization exercise that preserves

the internal coherence of their individual positions. Both statisticians

[Stone, 1961, Morris, 1977, Lindley, 1983, Clemen and Winkler, 1999] and

philosophers [Bovens and Rabinowicz, 2006, Hartmann and Sprenger, 2011] have

addressed this topic.

2.7 example: Prospecting

James and Claire, who both make investments in mining prospects, have been

told that samples from a region surveyed recently have mass fractions of titanium

averaging 3 g kg-1, give or take 1 g kg-1 (where “give or take” means that the

true mass fraction of titanium in the region sampled is between 2 g kg-1 and

4 g kg-1 with 95 % probability). James, however, has also been told that the

samples are of a sandstone with grains of ilmenite. On this basis, James may

assign a much higher probability than Claire to the proposition that asserts that

the region sampled includes an economically viable deposit of titanium

ore.

3 Probability Calculus

3.1 Axioms

Once numeric probabilities are in hand, irrespective of how they may

be interpreted, the same set of rules, or axioms, is used to combine

them. We formulate these axioms in the context where probability

is regarded as measuring degree of (rational) belief in the truth of

propositions, given a particular body of knowledge and universe of discourse,

, that

makes all the participating elements meaningful.

Let and

denote propositions

whose probabilities

and express

degrees of belief about their truth given (or, conditionally upon) the context defined by

. The notation

denotes the conditional

probability of , assuming

that is true and given

the context defined by .

Note that is not

necessarily 0 when :

for example, the probability is 0 that a point chosen uniformly at random over the

surface of the earth will be on the equator; yet the probability is ½ that,

conditionally on its being on the equator, its longitude is between 0° and 180°

West of the prime meridian at Greenwich, UK.

The axioms for the calculus of probability are these:

Convexity:

is a number between 0 and 1, and it is 1 if and only if

logically implies ;

Addition:

,

where the expression “

or ”

is true if and only if ,

,

or both are true;

Multiplication:

.

Since the roles of

and

are interchangeable, the multiplication axiom obviously can also be written as

.

Most accounts of mathematical probability theory use an additional rule

(countable additivity) that ensures that the probability that at least one

proposition is true, among countably infinitely many mutually exclusive

propositions, equals the sum of their individual probabilities [Casella and

Berger, 2002, Definition 1.2.4]. (“Countably infinitely many” means “as many as

there are integer numbers”.)

When the context that

defines is obvious, often one suppresses explicit reference to it, as in this derivation: if

denotes the

negation of ,

then Convexity and the Addition Rule imply that

because one

but not both of

and

must be true.

3.2 Independence

The concept of independence pervades much of probability theory. Two propositions

and

are independent if the probability that both are true equals

the product of their individual probabilities of being true. If

asserts that there is a Queen in Alexandra’s poker hand, and

asserts

that Beatrice’s comprises red cards only, both hands having been dealt from the same

deck, then

and

are independent. Intuitively, if knowledge of the truth of one proposition

influences the assessment of probability of another, then they are dependent:

in particular, two mutually exclusive propositions are dependent. If

, then

and

are independent

given .

3.3 Extending the Conversation

When considering the probability of a proposition, it often proves

advantageous to consider the truth or falsity of another one, somehow

related to the first [Lindley, 2006, §5.6]. To assess the probability

of a

positive tuberculin skin test (§3.6), it is convenient to consider how the test performs

separately in persons infected or not infected with Mycobacterium tuberculosis: if

denotes

infection, then

, where

is the probability of

a false positive, and

is the probability of a false negative, both more accessible than

.

3.4 Coherence

If an ideal reasoning agent (human or machine) assigns probabilities to events or

to the truth of propositions according to the foregoing axioms, then this agent’s

beliefs are said to be coherent. In these circumstances, if probabilities are used to

inform bets concerning the truth of propositions in the universe of discourse where

these probabilities are meaningful, then it is impossible (for a “bookie”) to devise

a collection of bets that bring an assured loss to this agent (a so-called “Dutch

Book”).

Now, suppose that, having ascertained the truth of a proposition

, one produces

as assessment of

’s truth on the evidence

provided by . Next,

one determines that ,

too, is true and revises this last assessment of

’s truth to

become .

The process whereby probabilities are updated is coherently extensible if the

resulting assessment is the same irrespective of whether the evidence provided by

and

is

brought to bear either sequentially, as just considered, or simultaneously. The

incorporation of information from multiple sources, and the corresponding

propagation of uncertainty, that is carried out by application of Bayes’ formula,

which is described next and illustrated in examples §3.6 and §6.7, is coherently

extensible.

3.5 Bayes’s Formula

If exactly one (that is, one and one only) among propositions

can be

true, and

is another proposition with positive probability, then

(1)

This follows from the axioms above because

(Multiplication axiom), whose numerator equals

(Multiplication axiom), and whose denominator equals

(“extending the conversation”, as in §3.3).

3.6 example: Tuberculin Test

Richard has been advised that his tuberculin skin test has returned a

positive result. The tuberculin skin test has a reported false-negative rate of

during the initial evaluation of persons with active tuberculosis

[American Thoracic Society, 1999, Holden et al., 1971]: this means

that the probability is 0.25 that the test will yield a negative

()

response when administered to an infected person

(),

.

Therefore, the probability is only 0.75 that infection will yield a positive test result.

In populations where cross-reactivity with other mycobacteria is common, the test’s

false-positive rate is 5%: that is, the conditional probability of a positive result

() for a person that

is not infected ()

is .

Richard happens to live in an area where tuberculosis has a prevalence of

.

Given the positive result of the test he underwent, the probability that he is

infected is

Common sense suggests that the diagnostic value of the test should depend on its

false-negative and false-positive rates, as well as on the prevalence of the disease:

Bayes’ formula states exactly how these ingredients should be combined to produce

,

which expresses that diagnostic value quantitatively.

Richard has the tuberculin skin test repeated, and this second test also turns out

positive. To incorporate this additional piece of evidence into the probability that

Richard is infected, first we summarize the state of knowledge (about whether he

is infected) determined by the result from the first test. This is done by defining

and

,

and using them in the role that the overall probability of infection

() or

non-infection ()

played prior to Richard’s first test, when all one knew about his condition was

that he was a member of a population where the prevalence of tuberculosis was

.

Again applying Bayes’ theorem, and assuming that the two tests are independent,

the revised probability that Richard is infected after two positive tests

is

If, instead, one had been initially told that Richard had had two independent,

positive tuberculin skin tests, then the calculation would have been:

This example illustrates the fact that Bayes’ theorem produces the same

probability irrespective of whether the information is incorporated sequentially, or

all at once.

3.7 Growth of Knowledge

The example in §3.6 illustrated how the probability of Richard being infected

increased (relative to the overall probability of infection in the town where he

lives) as a first, and then a second tuberculin test turned out positive. However,

even if he is infected, by chance alone a test may turn out negative. In a sequence

of tests, therefore, the probability of his being infected may oscillate, increasing

when a test turns out positive, decreasing when some subsequent test turns out

negative.

Therefore, the question naturally arises of whether a person employing the

Bayesian method of exploiting information, and incorporating it into the current

state of knowledge, ever will, in situations of uncertainty, arrive at conclusions

with overwhelming confidence. Jimmie Savage proved rigorously that the

answer is “yes” with great generality: “with observation of an abundance of

relevant data, the person is almost certain to become highly convinced of

the truth, and […] he himself knows this to be the case” [Savage, 1972,

§3.6].

The restriction to “relevant data” is critical: in relation with the tuberculin test, if it

happened that ,

then the test would have no discriminatory power, and in fact would be irrelevant

to learning about disease status.

4 Random Variables and Probability Distributions

4.1 Random Variables

The notion of random variable originates in games of chance, like roulette, whose

outcomes are unpredictable. Its rigorous mathematical definition (measurable

function from one probability space into another) is unlikely to be of great interest

to the metrologist. Instead, one may like to keep in mind its heuristic

meaning: the value of a quantity that has a probability distribution as an

attribute whose role is to describe the uncertainty associated with that

value.

4.2 example: Roulette

In the version of roulette played in Monte Carlo, the possible outcomes are numbers in

the set

(usually one disregards other possible, but “uninteresting” outcomes, including

those where the ball exits the wheel and lands elsewhere, or where it lands inside

the wheel but in none of its numbered pockets). Once those 37 numbers are

deemed to be equally likely, one can speak of a random variable that is equal to

with probability

, or that is odd

with probability .

(Note that these statements are meaningful irrespective of whether the event in

question will happen in the future, or has happened already, provided one does

not know its actual outcome yet).

4.3 example: Light Bulb

The GE A19 Party Light 25 W incandescent light bulb has expected lifetime

2000 h: this is usually taken to mean that, if a brand new bulb is turned on and

left on supplied with constant 120 V electrical current until it burns out, its actual

lifetime may be described as a realized value (realization, or outcome) of a random

variable with an exponential probability distribution (§4.10) whose expected value is

— this is

denoted

in §4.10, and in general it needs to be estimated from experimental data.

The concept of random variable applies just as well to domains of discourse

unrelated to games of chance, hence can be used to suggest uncertainty about the

value of a quantity, irrespective of the source of this uncertainty, including

situations where there is nothing “random” (in the sense of “chancy”) in

play.

4.4 Notational Convention

For the most part, upper case letters (Roman or Greek) denote generic quantity

values modeled as random variables, and their lowercase counterparts denote

particular values.

Upper case letters like

or ,

and ,

denote generic random variables, without implying that any of the former

necessarily play the role of input quantity values (as defined in the international

vocabulary of metrology (VIM) Joint Committee for Guides in Metrology [2008c],

VIM 2.50), or that the latter necessarily plays the role of output quantity values

(VIM 2.51) in a measurement model (VIM 2.48).

The probabilities most commonly encountered in metrological practice

concern sets of numbers that a quantity value may take: in this case, if

denotes a random variable whose values belong to a set

, and

is a subset

of , then

denotes the

probability that ’s

value lies in .

For example, if

represents the length (expressed in meter, say) of a gauge block, then

would be the set of all possible values of length, and

could

be the subset of such values between 0.0423 m and 0.0427 m, say.

4.5 Probability Distributions

Given a random variable one

can then define a function

such that for all

to which a probability

can be assigned. This

is called ’s

probability distribution.

If

is countable (that is, either finite or infinite but with as many

elements as there are positive integers), then one says that

has a

discrete distribution, which is fully specified by the probability it assigns to each

value in .

For example, the outcome of a roulette wheel is a random variable whose

probability distribution is discrete.

If is

uncountable (that is, it has as many elements as there are real numbers) and

for all

, then one

says that

has a continuous distribution. For example, the lifetime of an incandescent light

bulb that does light up and then is constantly left on until it burns out is a

random variable with a continuous distribution.

A distribution may be neither discrete nor continuous, but of a mixed type

instead: for example, when a random variable is equal to 0 with probability

,

and has an exponential distribution (see §4.10) with probability

.

Since a brand new light bulb has a positive probability of burning out the instant

it is turned on, its lifetime may more realistically be modeled as a random

variable that has an “atom” of probability at 0, and is exponential with the

complementary probability.

4.6 Probability Distribution Function

The probability distribution of a random variable

whose possible values are real numbers, can be succinctly described

by its probability distribution function, which is the function

such that

for every

real number .

Note that the symbol we use here to denote the probability distribution function,

is the same that we used in §4.5 to denote the probability distribution itself. Any

confusion this may cause will be promptly resolved by examining the argument of

: if it

is a set, then we mean the distribution itself, while if it is a number or a vector

with numerical components, then we mean the probability distribution

function.

For example, if is real-valued

and is a particular

real number, then in

the

on the left hand side refers to the probability distribution function, while the

on the right hand side refers to the distribution itself because

denotes the set of all real numbers no greater than

.

Since the distribution function determines the distribution, the confusion is

harmless.

4.7 Probability Density Function

If

has a discrete distribution (§4.5), then its probability density

(also known as its probability mass function) is the function

such

that

for .

If is uncountable

and ’s

distribution is continuous and sufficiently smooth (in the sense described next),

then the corresponding probability density function (PDF) is defined similarly to a

material object’s mass density, as follows.

Consider the simplest case, where

is an interval of real numbers, and suppose that

is one point in the interior of this interval. Now suppose that

is an infinite sequence of positive numbers decreasing to zero. If

’s

probability distribution is sufficiently smooth, then the limit

exists. The

function so

defined is ’s

probability density function. If the distribution function is differentiable, then the

probability density is the derivative of the probability distribution function,

.

Both the probability distribution function and the probability density function

have multivariate counterparts.

4.8 Expected Value, Variance, and Standard Deviation

The expectation (expected value, or mean value) of a (scalar or vector valued) function

of a random

variable

is if

has a continuous probability distribution with density

, or

if

has a discrete

distribution. Note that

can be computed without determining the probability distribution of the random

variable

explicitly.

indicates

’s

location, or the center of its probability distribution: therefore it is a

most succinct summary of this distribution, and it is the best estimate of

’s

value in the sense that it has the smallest mean squared error.

The median is another indication of location for a scalar random variable: it is any

value such

that

and ,

and it need not be unique. The median is the best estimate of

’s

value in the sense that it has the smallest absolute deviation.

Neither the mean nor the median need be “representative” values of the distribution. For

example, when

denotes a proportion whose most common values are close to 0 or to 1 and

its mean is close to ½, then values close to the mean are very unlikely.

need not exist (in the sense that the defining integral or sum may fail to

converge).

, where

is a positive

integer, is called ’s

th moment. The

variance of

is ,

or, equivalently, the difference between its second moment and the

square of its first moment. The positive square root of the variance,

, is the standarddeviation of .

4.9 example: Poisson Distribution

The only values that a Poisson distributed random variable

can

take are the non-negative integers: 0, 1, 2, …, and the probability that its value is

is

, where

is some given

positive number, and .

This model distributes its unit of probability into infinitely

many lumps, one at each non-negative integer, so that

decreases rapidly

with increasing ,

and .

Both the expected value and the variance equal

. The

number of alpha particles emitted by a sample containing the radionuclide

, during a

period of

seconds that is a small fraction of this isotope’s half-life (138 days),

is a value of a Poisson random variable with mean proportional to

.

4.10 example: Exponential Distribution

Suppose that

represents the lifetime (thousands of hours) of an incandescent light bulb, such that,

for ,

, for some given

number : note that, as

decreases toward 0, and

increases without limit,

approaches 1. Focus on

a particular number ,

and consider the ratio

for some . As

decreases to

this ratio approaches

. Therefore,

the function

such that is the

probability density of the exponential distribution. In this case, the probability distribution

function is

such that .

’s mean value

is , and its

variance is .

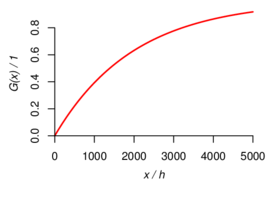

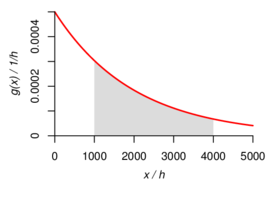

Figure 1 illustrates both the distribution function and the density for the case where

.

Figure 1: Exponential Distribution with Mean 2000 h. The left

panel shows a portion of the graph of the probability distribution

function. The right panel shows the corresponding portion of the graph

of the probability density function. The area of the shaded region

equals the probability of a value between 1000 h and 4000 h: this is

.

Note that the vertical scales in the left and right panels are different.

4.11 Joint, Marginal, and Conditional Distributions

Suppose that

represents a bivariate quantity value, for example, the Cartesian coordinates

of a point inside a circle of unit radius centered at

. In this case

the range

of

is this unit circle. The joint probability distribution of

and

describes a state of knowledge about the location of

: for example, that

more likely than not

is less than ½ away from the center of the circle: statements of this kind involve

and

together (that is, jointly).

The marginal probability distributions of

and

are

the probability distributions that characterize the state of knowledge about each

of them separately from the other: for example, that more likely than not

, irrespective

of .

Clearly, the marginal distributions have to be consistent with the joint

distribution, and while it is true that the joint distribution determines the

marginal distributions, the reverse is not true, in that typically there

are many joint distributions consistent with given marginal distributions

[Possolo, 2010].

Now, suppose one knows that .

This implies that , hence

that is somewhere

on a particular chord

of the unit circle. The conditional probability distribution of

given

that

is a (univariate) probability distribution over this chord.

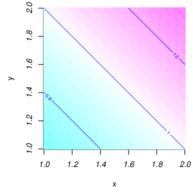

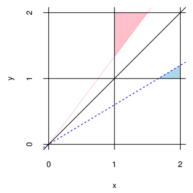

4.12 example: Shark’s Fin

The random variables

and take values in the

interval and have joint

probability density function

such that for

and is zero otherwise

(Figure 2): since

and ,

is a

bona fide (bivariate) probability density.

The density of the marginal distribution of

is

, and

similarly for .

And the density of the conditional distribution of

given

is

.

To determine the probability density of

, also depicted in

Figure 2, note that .

First, consider the case :

and

. Next, consider

the case :

and

.

Figure 2: Shark’s Fin. The left panel shows

the probability density of the joint distribution of

and

defined in §4.12. In the middle panel, the dashed (blue) line has slope

,

and the points inside the small (blue) triangle

have coordinates that satisfy the conditions

and .

The dotted (red) line has slope ,

and the points inside the large (red) triangle

have coordinates that satisfy the conditions

and .

The right panel shows the probability density function of

.

4.13 Independent Random Variables

The (scalar or vectorial) random variables

and

are independent

if and only if

for all

subsets

and

in their respective ranges (to which probabilities can be coherently assigned.)

Suppose

and

have joint probability distribution with probability density function

, and marginal

density functions

and :

the random variables are independent if and only if

.

4.14 example: Unit Circle

Suppose that the probability distribution of a point is

uniform inside the circle of unit radius centered at the origin

of the

Euclidean plane. This means that the probability that a point with Cartesian coordinates

should lie in a subset

of this circle is proportional

to ’s area, but is otherwise

independent of ’s

shape or location within the circle. The probability density function of the joint distribution

of and

is the

function

such that

if , and

otherwise. The

random variables

and

are dependent (§4.13): for example, if one is told that

, then one can surely

conclude that . The

marginal distribution of

has density

such that

for .

has expected value 0 and standard deviation ½. Owing to symmetry,

and

have

identical marginal distributions.

4.15 Correlations and Copulas

If two or more of the random variables are dependent, then modeling their

individual probability distributions will not suffice to specify their joint behavior:

their joint probability distribution is needed.

One commonly used metric of dependence between two random variables

and

is Pearson’s product-moment correlation coefficient, defined as

.

However, it is possible for the variables to be dependent and still have

.

When the only information in hand are the expected values, standard deviations,

and correlations, and still one needs a joint distribution consistent with this

information, then the usual course of action is to assign distributions to them

individually, and then manufacturing a joint distribution using a copula

[Possolo, 2010] — there is, however, a multitude of different copulas that can be

used for this purpose, and the choice that must be made generally is

influential.

5 Functions of Random Variables

5.1 Overview

If a random variable

is a function of other random variables,

, then

and the joint probability

distribution of determine the

probability distribution of .

If only the means, standard deviations, and correlations of

are known,

then it still is possible to derive approximations to the mean and standard deviation

of , by

application of the Delta Method.

If the joint probability distribution of

is

known, then it may be possible to determine the probability distribution of

analytically, using the change of variables formula.

In general, it is possible to obtain a sample from

’s

distribution by taking a sample from the joint distribution of

and

applying

to each element of this sample (§5.8). The results may then be summarized in

several different ways: one of them is an estimate of the probability density of

[Silverman, 1986], a procedure that is implemented in function density of the R

environment for statistical programming and graphics [R Development Core

Team, 2010].

5.2 Delta Method

If is a random

variable with mean

and variance ,

is a

differentiable real-valued function of a real variable whose first derivative does not

vanish at ,

and ,

then ,

and .

(This results from the so-called Taylor approximation that replaces

by a straight line

tangent to its graph at .)

If is an

average of independent, identically distributed random variables with finite variance, then

also is approximately

Gaussian with mean

and standard deviation ,

where

denotes the absolute value of the first derivative of

evaluated

at .

The quality of the approximation improves with increasing

.

5.3 Delta Method — Degeneracy

When and

exists and

is not zero,

is an average of independent, identically distributed random variables with finite variance,

and

is large, then the probability distribution of

is approximately

like that of , where

denotes a Gaussian

(or, normal) random variable with mean 0 and standard deviation 1. Since the variance of

is 2, the standard

deviation of is

approximately ,

rather different from what applies in the conditions of §5.2.

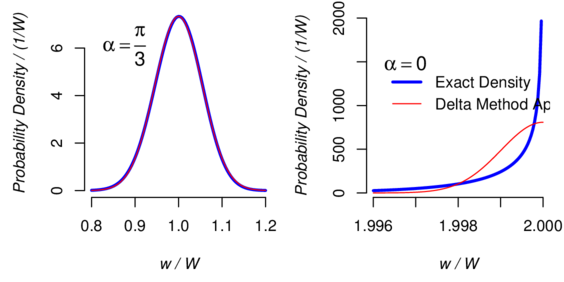

5.4 example: Radiant Power

Consider a surface whose reflectance is Lambertian: that is, light falling on it is

scattered in such a way that the surface’s brightness apparent to an observer is

the same regardless of the observer’s angle of view. The radiant power

emitted by such surface that is measured by a sensor aimed at angle

to the surface’s normal

is proportional to ,

hence one writes

[Cannon, 1998, Köhler, 1998].

If knowledge about the value of

is modeled by a Gaussian distribution with mean

and standard

measurement uncertainty

(both expressed in radians), then §5.2 (with

) suggests that

knowledge of

should be described approximately by a Gaussian distribution with mean

and standard

measurement uncertainty .

If, for example, ,

, and

, then the

approximation to ’s

distribution that the Delta Method suggests, of a Gaussian distribution with mean

and standard

deviation ,

is remarkably accurate (Figure 3).

When the detector is aimed squarely at the target, that is

, this

approximation no longer works because the first derivative of the cosine vanishes

at ,

which is the degenerate case that §5.3 contemplates. In this case,

’s

standard measurement uncertainty is approximately

. For

and

, this

equals ,

which is accurate to the two significant digits shown. However, Figure 3 shows

that, in this case, the Delta Method produces a poor approximation.

When , the

probability density of

is markedly asymmetrical, and the meaning of

’s

standard deviation is rather different from its meaning when

. Indeed,

when the

probability that

should lie within one standard deviation of its expected value is

approximately.

Figure 3: Radiant Power. Probability density of the radiant power

emitted by a Lambertian surface that is

measured by a sensor aimed at an angle

to the surface’s normal, when

has a Gaussian distribution with mean

(left panel) or

(right panel), and standard deviation .

In both cases, the thick blue line is the exact density, and the thin red line

is the Delta Method approximation.

5.5 Delta Method — Multivariate

The Delta Method can be extended to apply to a function of several random variables.

Suppose that ,

…,

are averages of sets of random variables whose variances are finite. The

variables in each set are independent and identically distributed, those in set

having

mean and

variance .

However, variables in different sets may be dependent, hence the

may be dependent,

too. Let denote the

symmetrical matrix

whose element

is the covariance

between

and ,

for .

Now, consider the random variable ,

where denotes a

real-valued function of

variables whose first partial derivatives are continuous and none vanishes at

. If

is finite, then

also is approximately

Gaussian with mean

and variance .

If are uncorrelated

and have means and

standard deviations ,

then the Delta Method approximation reduces to a well-known

formula first presented by Gauss [Gauss, 1823, §18, Problema]:

, where the sensitivitycoefficient is

the value at of

the th partial

derivative of

with respect to .

5.6 example: Beer-Lambert-Bouguer Law

If a beam of monochromatic light of power

(W) travels a

path of length

(m) through a solution containing a solute whose molar absorptivity for that light

is

(L mol-1 m-1), and whose molar concentration is

(mol L-1), then the beam’s power is reduced to

(W) such that

. Application of Gauss’s

formula (§5.5) to

yields:

5.7 example: Darcy’s Law

Darcy’s law relates the dynamic viscosity

of a fluid to the volumetric

rate of discharge

(volume per unit of time) when the fluid flows through a permeable cylindrical medium of cross-section

and intrinsic

permeability under

a pressure drop of

along a length ,

as follows: .

To compute an approximation to the standard deviation of

, one may use

the formula from §5.5 directly, or first take the logarithm of both sides, which linearizes the

relationship, .

Applied to these logarithms, the formula from §5.5 is exact. The approximation is

then done for each term separately, using the univariate Delta Method.

Since ,

and similarly for the other logarithmic terms,

.

In other words, the square of the coefficient of variation of

is

approximately equal to the sum of the squares of the variation coefficients of the

other variables.

5.8 Monte Carlo Method

The Monte Carlo method offers several important advantages over the Delta

Method described in §5.2 and §5.5: (i) it can produce as many correct

significant digits in its results as may be required; (ii) it does not involve the

computation of derivatives, either analytically or numerically; (iii) it is

applicable in many situations where the Delta Method is not; (iv) it provides a

picture of the whole probability distribution of a function of several random

variables, not just an approximation to it, or to its mean and standard

deviation.

The Monte Carlo method in general dates back to the middle of the twentieth

century [Metropolis and Ulam, 1949, Metropolis et al., 1953]. A variant used in

mathematical statistics is known as the parametric bootstrap [Efron and

Tibshirani, 1993]. This involves using random draws from a (possibly

multivariate) probability distribution whose parameters have been replaced by

estimates thereof (for example, means of posterior probability distributions, §6) to

ascertain the probability distribution of a function of one (or more) random

variables. Morgan and Henrion [1992] and Joint Committee for Guides in

Metrology [2008b] describe how it may be employed to evaluate measurement

uncertainty, and provide illustrative examples.

The procedure comprises the following steps:

MC1

Define the joint probability distribution of ,

…, .

MC2

Choose a suitably large positive integer

and draw a sample of size

from this joint distribution to obtain ,

…, .

(If ,

…,

happen to be independent, then this amounts to drawing a sample of

size

from the distribution of each of them separately.)

MC3

Compute ,

…, ,

which are a sample from ’s

distribution.

MC4

Summarize this sample in one or more of these different ways:

MC4.a — Probability Density

The most inclusive summarization

is in the form of an estimate of ’s

probability density function: this may be either a simple histogram,

or a kernel density estimate [Silverman, 1986].

MC4.b — Mean and Standard Deviation

The mean and standard

deviation of

are estimated by the mean and the standard deviation of .

(To ascertain the number of significant digits in this mean and

standard deviation, hence to decide whether

is large enough for the intended purpose, or should be increased,

one may employ either the adaptive procedure explained in the

Supplement 1 to the GUM [Joint Committee for Guides in Metrology, 2008b,

7.9], or resort to the non-parametric statistical bootstrap or to

other resampling methods [Davison and Hinkley, 1997].)

MC4.c — Probability Interval

If

denote the result of ordering

from smallest to largest, then the interval

includes ’s

true value with probability .

(Since

and

need not be integers, the end-points of this coverage interval may

be calculated by interpolation of adjacent s.)

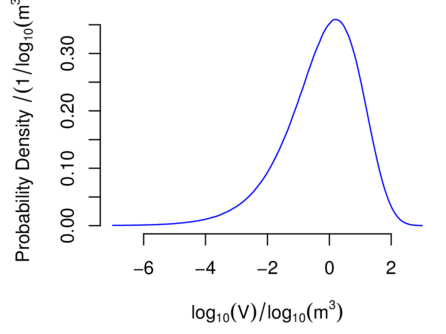

5.9 example: Volume of Cylinder

The radius

and the height

of a cylinder are values of independent random variables with exponential probability

distributions with mean 1 m. To characterize the probability distribution of its volume

, draw a sample of

size from the joint

distribution of

and ,

and compute the volume corresponding to each pair of sampled values

to obtain a sample of the same size from the distribution of

. The

average and standard deviation of these values are 6.3 m3 and 21 m3, and they are

estimates (whose two most significant digits are exact) of the mean and standard

deviation of .

Figure 4 depicts an estimate of the corresponding probability density.

Figure 4: Cylinder Volume. Kernel density estimate [Silverman, 1986] of

the probability density of the volume of a cylinder whose radius and height are

realized values of independent, exponentially distributed random variables

with mean 1 m.

5.10 Change-of-Variable Formula — Univariate

Suppose that

is a random variable with a continuous distribution and values in

, with probability distribution

function and probability

density function , and

consider the random variable

where

denotes a real-valued function of a real variable. Let

denote the set

where takes its

values, and let

and

denote ’s

probability distribution function and probability density function, respectively. In

these circumstances [Casella and Berger, 2002, Chapter 2].

If

is increasing on

and

denotes its inverse, then

for ;

and if

is decreasing, then .

If

is either increasing or decreasing on

(but not both), and its inverse

has a continuous first derivative ,

then ,

for ,

where

denotes the absolute value of the derivative of

at .

5.11 example: Oscillating Mirror

A horizontal beam of light emerges from a tiny hole in a wall and travels along a

1 m long path at right angles to the wall, towards a flat mirror that oscillates

freely around a vertical axis. When the mirror’s surface normal makes an angle

with the beam, its reflection hits the wall at distance

from

the hole (positive to the right of the hole and negative to the left). If

is uniformly (or, rectangularly) distributed between

and

, then

, and

’s probability

density is

such that

for .

As it turns out, both the mean and the standard deviation of

are

infinite [Feller, 1971, Page 51].

5.12 Change-of-Variable Formula — Multivariate

Suppose that are random

variables and consider

for , and where

are real-valued

functions of

real variables each.

Suppose also that (i) the vector

takes values in an open subset

of -dimensional

Euclidean space, and has a continuous joint probability distribution with probability density function

; (ii) the vector-valued

function is invertible,

and the inverse has a

Jacobian determinant

that does not vanish on .

CV1

Solve the

equations ,

…, ,

for ,

to obtain the inverse transformation such that ,

…, .

CV2

Find , the partial

derivative of with

respect to its th

argument, for ,

and compute the Jacobian determinant of the inverse transformation at

:

CV3

The density the joint probability distribution of the random vector

is

such that

(2)

Note that is

a scalar, and

denotes its absolute value.

CV4

The probability density of

is , where the

integrals are over

the ranges of .

5.13 example: Linear Combinations of Gaussian Random Variables

Suppose that

and

are independent, Gaussian random variables with mean 0 and variance 1, and let

, and

, for given real

numbers and

. The inverse

transformation maps

onto , and has Jacobian

determinant whose

absolute value is .

Since the density of the joint probability distribution of

and

is

,

application of the multivariate change-of-variable formula yields

But this means that

and

also are independent and Gaussian with mean 0 and variance

.

On the one hand, this result is surprising because

and

both are functions of the same random variables. On the other hand it is

hardly surprising because the transformation amounts to a rotation of the

coordinate axes, followed by a global dilation. Since the joint distribution of

and

is circularly symmetric

relative to , so will the

joint distribution of

and

be, which implies independence and the same functional form for the density, up

to a difference in scale.

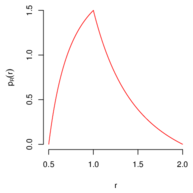

5.14 example: Ratio of Exponential Lifetimes

To compute the probability density of the ratio

of two independent and exponentially distributed random variables

and

with mean

, define the

function such that

, whose inverse is

, with Jacobian

determinant .

The multivariate change-of-variable formula then yields

for the density of the

joint distribution of

and . The (marginal)

density of

is , for

,

being 0 otherwise.

indeed is a probability density function because it is a non-negative function and

. However, since

, neither the mean

nor the variance of

is finite. The Delta Method, however, would have suggested that

and

that the coefficient of variation (ratio of the standard deviation to the mean) of

is

approximately.

5.15 example: Polar Coordinates

The inverse of the transformation that maps the polar coordinates

of a point in the Euclidean plane to its Cartesian coordinates

is

such

that for

and

, with Jacobian

determinant .

If and

are

independent Gaussian random variables with mean 0 and variance 1, then the probability

density of

is . Since

, it follows

that

and

are independent, the former having a Rayleigh distribution with mean

, the latter a uniform

distribution between

and .

6 Statistical Inference

The statistical inferences we are primarily interested in are probabilistic

statements about the unknown value of a quantity, produced by application of a

statistical method. In the example of §6.6, one of the inferences is this statement:

the probability is 95% that the difference between the numbers of hours gained withthe two soporifics is between 0.7 h and 2.5 h.

Another common inference is an estimate of the value of a quantity, which must be

qualified with an assessment of the associated uncertainty. In the example of §6.8, a

typical inference of this kind would be this: the difference in mean levels of thyroxinein the serum of two groups of children diagnosed with hypothyroidism is estimated aswith standarduncertainty

(Figure 6).

In our treatment of this example, the inference is based entirely on a small set of

empirical data, and on a particular choice of statistical model used to describe the

dispersion of the data, and to characterize the fact that no knowledge other than

the data was brought into play.

Statistical methods different from the one we used could have been employed:

some of these would produce the same result (in particular those illustrated when

this dataset was first described [Student, 1908, Fisher, 1973]), while others would

have produced different results.

Even when the result is the same, it may be variously interpreted:

For some that statement means that if the same sampling and study

method is used repeatedly, and each time the resulting dataset is

modeled and analyzed in the same way to produce an interval like the

one above, then about 95 % of the resulting intervals will include the

true difference sought — with no guarantee or implication that the

interval that was obtained is one of these;

For others (among whom we stand) that statement expresses the degree

of belief one is entitled to have about the true difference lying between

0.7 h and 2.5 h specifically, in light of all the relevant information in

hand.

6.1 Bayesian Inference

Bayesian inference [Bernardo and Smith, 2000, Lindley, 2006, Robert, 2007] is a

class of statistical procedures that serve to blend preexisting information about

the value of a quantity with fresh information in empirical data.

The defining traits of a Bayesian procedure are these:

(i)

All quantity values that are the objects of interest but are accessible

to direct observation (non-observables) are modeled as values of

non-observable random variables whose (prior, or a priori) distributions

encode and convey states of incomplete knowledge about those values;

(ii)

The empirical data (observables) are modeled as realized values of

random variables whose probability distributions depend on those

objects of interest;

(iii)

Preexisting information about those objects of interest is updated in

light of the fresh empirical data by application of Bayes rule, and the

results are encapsulated in a (posterior, or a posteriori) probability

distribution;

(iv)

Selected aspects of this distribution are then abstracted from it and

used to characterize the objects of interest and to describe the state of

knowledge about them.

6.2 Prior Distribution

Let denote

the value of the quantity of interest, which we model as realized value of a random variable

with probability density

function that encodes the

state of knowledge about

prior to obtaining fresh data, and which must be defined even if there is no prior

knowledge.

Defining such

often is a challenging task. If in fact there exists substantial prior knowledge about

, then

it needs to be elicited from experts in the matter and encapsulated in the form of

a particular probability density: Garthwaite et al. [2005] review how

this may be done. For example, when measuring the mass fraction of

titanium in a mineral specimen, then knowledge of the species (ilmenite,

titanite, rutile, etc.) of the specimen is highly informative about that mass

fraction. Familiarity with the process of analytical chemistry employed

to make the measurement may indicate the dispersion of values to be

expected.

In some cases, essentially no prior knowledge exists about

, or

none is deemed reliable enough to be taken into account. In such cases, a so-called

non-informative prior distribution needs to be produced and assigned to

that reflects this

state of affairs: if

is univariate (that is, a single number), then the rules developed by Jeffreys [1961] often prove

satisfactory; if

is multivariate (that is, a numerical vector), then the so-called reference prior

distributions are recommended [Bernardo and Smith, 2007] (these reduce to

Jeffreys’s in the univariate case).

These rules often produce a that

is improper, in the sense that

diverges to infinity, where

denotes the range of .

(If

should have a discrete distribution then this integral is replaced by a sum.)

Fortunately, once used in Bayes Rule (§3.5 and §6.4), improper priors often lead

to proper posterior probability distributions.

6.3 Likelihood Function

The empirical data

(which may be a single number, a numerical vector, or a data structure of still

greater complexity) are modeled as realized values of a random variable

whose probability density describes the corresponding dispersion of values.

This density must depend on ,

which is another way of saying that the data are informative about

(otherwise there would be nothing to be gained by observing them). In

fact, this is the density of the conditional probability distribution of

given

that .

Choosing a specific functional form for it generally is a non-trivial exercise: it

involves defining a statistical model that correctly captures the dispersion of

values likely to be obtained in the experiment that produces them.

Once the data are

in hand, becomes a

function of alone, being

largest for values of

that make the data appear most likely. As such, it still is non-negative, but its integral (or

sum, if ’s

distribution should be discrete) over the range of

, need

not be 1.

6.4 Posterior Distribution

Suppose that both

given that and

have continuous

distributions with densities

and .

In these circumstances, Bayes rule becomes

(3)

The function , which is

defined over the range of

for each fixed value ,

is the density of the posterior distribution of the value of the quantity of interest

given

the data.

In some cases this can be computed in closed form, in many others it cannot. In

all cases it is possible to obtain a sample from this posterior distribution by

application of a procedure known as Markov Chain Monte Carlo (MCMC)

[Gelman et al., 2003]. This sample can then be summarized as described in

§5.8.

6.5 example: Viral Load

Once infected by influenza A virus, an epithelial cell of the upper respiratory tract

releases

virions on average, which may then go on to infect other cells. This number

depends

on the volume of the cell, and we will treat it as realized value of a non-observable

random variable with an exponential distribution whose expected value,

for some

, is known.

Given ,

the actual number of virions that are released is

,

and this is like a realized value of a Poisson random variable with mean

.

Suppose that the prior density is ,

and the likelihood function is ,

for . The posterior

distribution of

given

belongs to the gamma family, and has expected value

, variance

, and

density

6.6 example: Sleep Hours

The differences between the numbers of additional hours of sleep that ten patients

gained when using two soporific drugs, described in examples given by

Student [1908] and [Fisher, 1973, §24], were 1.2 h, 2.4 h, 1.3 h, 1.3 h, 0.0 h, 1.0 h,

1.8 h, 0.8 h, 4.6 h, and 1.4 h.

Suppose that, given

and ,

these are realized values of independent Gaussian random variables with mean

and variance

. Let

denote their

average, and

denote the sum of their squared deviations from

divided by 9. In these circumstances, the likelihood function is

.

Assume, in addition, that

and

are realized values of non-observable random variables

and

that are independent

a priori and such that

and are uniformly

distributed between

and

(both improper prior distributions). Then, given

and

,

is like a realized value of a random variable with a Student’s

distribution

with degrees

of freedom, and

is like a realized value of a random variable with a chi-squared distribution with

degrees of freedom [Box and Tiao, 1973, Theorem 2.2.1].

Therefore, the expected value of the posterior distribution

of the mean difference of hours of sleep gained is

, and the standard

deviation is . A 95 %

probability interval for

ranges from 0.7 h to 2.5 h, and a similar one for

ranges from 0.8 h to 2.2 h.

Suppose that

and are the

counterparts of

and

once the information in the data has been taken into account:

that is, their probability distribution is the joint (or, bivariate)

posterior probability distribution given the data. Even though

and

were assumed to be

independent a priori,

and

turn out to be dependent a posteriori (that is, given the data), but their

correlation is zero [Lindley, 1965b, §5.4].

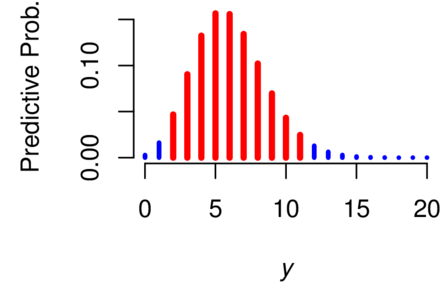

6.7 example: Hurricanes

A major hurricane has category 3, 4, or 5 on the Saffir-Simpson Hurricane Scale

[Simpson, 1974]: its central pressure is no more than 945 mbar (94 500 Pa), it has winds

of at least

(49.6 m s-1), generates sea surges of 9 feet (2.7 m) or greater, and has the

potential to cause extensive damage.

The numbers of major hurricanes that struck the U.S. mainland directly, in

each decade starting with 1851–1860 and ending with 1991–2010, are:

6, 1, 7, 5, 8, 4, 7, 5, 8, 10, 8, 6, 4, 4, 5, 7 [Blake et al., 2011]. Let

denote the number of decades,

denote the corresponding

counts, and . Suppose that

one wishes to predict ,

the number of such hurricanes in the decade 2011–2020.

Assume that the mean number of such hurricanes per decade will have remained constant

between 1851 and 2010 (certainly a questionable assumption), with unknown value

, and that, conditionally

on this value, ,

…, ,

and

are realized values of independent Poisson random variables

, …,

(observable),

(non-observable), all with

mean value : their common

probability density is

for .

This model is commonly used for phenomena that result from the cumulative

effect of many improbable events [Feller, 1968, XI.6b].

Even though the goal is to predict ,

the fact that there is no a priori knowledge about

other than

that it must be positive, requires that this be modeled as the (non-observable) value of a

random variable

whose probability distribution must reflect this ignorance. (According to the

Bayesian paradigm, all states of knowledge, even complete ignorance, have to be

modeled using probability distributions.)

If the prior distribution chosen for

is the reference prior distribution [Berger, 2006, Bernardo, 1979, Bernardo

and Smith, 2000], then the value of its probability density

at

should be

proportional to

[Bernardo and Smith, 2000, A.2], an improper prior probability

density. However, the corresponding posterior distribution for

is proper, in fact it is a gamma distribution with expected value

and probability

density function

such that

(4)

However, what is needed for the aforementioned prediction is the conditional distribution

of given

the observed counts: the so-called predictive distribution [Schervish, 1995, Page 18].

If

denotes the corresponding density, then

This defines a discrete probability distribution on the non-negative integers, often called

a Poisson-gamma mixture distribution [Bernardo and Smith, 2000, §3.2.2]. For our data,

since achieves

a maximum at

(Figure 5), this is the (a posteriori) most likely number

of major hurricanes

that will hit the U.S. mainland in 2011–2020. The mean of the posterior distribution is

. Since the probability

is 0.956 that ’s

value lies between 2 and 11 (inclusive), the interval whose end-points are 2 and 11 is a

coverage

interval for .

Figure 5: Hurricanes. Predictive probabilities for the number of major

hurricanes that

will hit the U.S. mainland in 2011–2020. The vertical axis indicates values of

from equation (5). The most likely number is 5, the expected number is

6, and the probability is 0.956 that the number will be between 2 and 11

(inclusive) (red bars).

6.8 example: Hypothyroidism

[Altman, 1991, Table 9.6] lists measurement results from Hulse et al. [1979], for

the concentration of thyroxine in the serum of sixteen children diagnosed

with hypothyroidism, of which nine had slight or no symptoms, and the

other seven had marked symptoms. The values measured for the former,

all in units of nmol/L, were 34, 45, 49, 55, 58, 59, 60, 62, and 86; and

for the latter they were 5, 8, 18, 24, 60, 84, and 96. The averages are

and

, and the standard

deviations are

and .

Our goal is to produce a probability interval for the difference between the corresponding

means,

and ,

say, when nothing is assumed known a priori either about

these means or about the corresponding standard deviations,

and

,

which may be different.

Given the values of these four parameters, suppose that the values measured in the

children with

slight or no symptoms are observed values of independent Gaussian random variables

with common

mean and standard

deviation , and that

those measured in the

children with marked symptoms are observed values of independent Gaussian random variables

, also independent

of the , with

common mean and

standard deviation .

The problem of constructing a probability interval for

under these circumstances is known as the Behrens-Fisher problem

[Ghosh and Kim, 2001]. For the Bayesian solution, we regard

,

,

and

as realized values of non-observable random variables

,

,

, and

, assumed independent

a priori and such that ,

,

, and

all

are uniformly distributed over the real numbers (hence have improper prior

distributions). The corresponding posterior distributions all are proper provided

and

.

However, the density of the posterior probability distribution of

given

the data cannot be computed in closed form.

This problem in Bayesian inference, and other problems much more demanding

than this, can be solved using the MCMC sampling technique mentioned in

§6.4, for which there exist several generic software implementations: we

obtained the results presented below using function metrop of the R package

mcmc [Geyer, 2010]. Typically, all that is needed is the logarithm of the

numerator of Bayes formula (3). Leaving out constants that do not involve

,

,

or

, this

is

MCMC produces a sample of suitably large size

from the joint posterior

distribution of ,

,

, and

, given the

data, say ,

…, .

The 95 % probability interval for the difference in mean levels of

thyroxine in the serum of the two groups, which extends from

to

, and Figure 6, are based

on a sample of size .

The probability density in this figure, and that probability interval, were computed

as described in MC4.c and MC4.d of §5.8, only applied to the differences

.

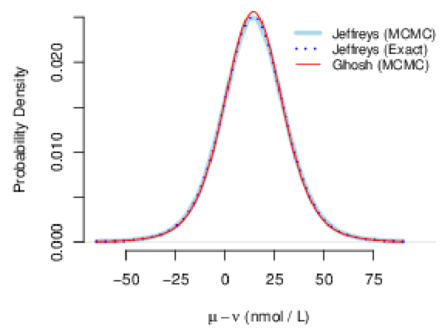

Figure 6: Hypothyroidism. Probability density of the posterior

distribution of the difference in mean levels of thyroxine in the serum

of two groups of children diagnosed with hypothyroidism: computed

via MCMC using either Jeffreys’s prior or the “matching” prior of

Ghosh and Kim [2001], alongside the exact version corresponding

to Jeffreys’s prior. The posterior mean and standard deviation are

and .

In this particular case it is possible to ascertain the correctness of the results owing to an

interesting, albeit surprising result: the posterior means are independent a posteriori,

and have probability distributions that are re-scaled, shifted versions of Student’s

distributions

with

and

degrees of freedom [Box and Tiao, 1973, 2.5.2]. Therefore, by application of the Monte

Carlo method of §5.8, one may obtain a sample from the posterior distribution of the

difference

independently of the MCMC procedure: the results are depicted in Figure 6

(where they are labeled “Jeffreys (Exact)”), and are essentially indistinguishable

from the results of MCMC.

This same figure shows yet another posterior density that differs hardly

at all from the posterior density corresponding to Jeffreys’s prior: this

alternative result corresponds to the “matching” prior distribution (also

improper) derived by Ghosh and Kim [2001], whose density is proportional to

. This

illustrates a generally good practice: that the sensitivity of the results of Bayesian

analysis should be evaluated by comparing how they vary when different but

comparably acceptable priors are used.

7 Acknowledgments

Antonio Possolo thanks colleagues and former colleagues from the Working Group

1 of the Joint Committee for Guides in Metrology, who offered valuable

comments and suggestions in multiple discussions of an early draft of a

document that he had submitted to the consideration of this Working

Group and that included material now in the present document: Walter

Bich, Maurice Cox, René Dybkær, Charles Ehrlich, Clemens Elster,

Tyler Estler, Brynn Hibbert, Hidetaka Imai, Willem Kool, Lars Nielsen,

Leslie Pendrill, Lorenzo Peretto, Steve Sidney, Adriaan van der Veen,

Graham White, and Wolfgang Wöger. Antonio Possolo is particularly

grateful to Tyler Estler for suggestions regarding §2.3 and §3.1, and to

Graham White for suggestions and corrections that greatly improved §3.6, on

the tuberculin test. Both authors thank their common NIST colleagues

Andrew Rukhin and Jack Wang for suggesting many corrections and

improvements. Mary Dal-Favero and Alan Heckert, both from NIST,

kindly facilitated the deployment of this material on the World Wide

Web.

References

D. G. Altman. Practical Statistics for Medical Research. Chapman &

Hall/CRC, Boca Raton, FL, 1991. Reprinted 1997.

American Thoracic Society. Diagnostic standards and classification of

tuberculosis in adults and children. American Journal of Respiratory andCritical Care Medicine, 161:1376–1395, 1999.

J. Berger. The case for objective Bayesian analysis. Bayesian Analysis,

1(3):385–402, 2006. URL http://ba.stat.cmu.edu/.

J. Bernardo and A. Smith. Bayesian Theory. John Wiley & Sons, New

York, 2000.

J. Bernardo and A. Smith. Bayesian Theory. John Wiley & Sons,

Chichester, England, 2nd edition, 2007.

J. M. Bernardo. Reference posterior distributions for Bayesian inference.

Journal of the Royal Statistical Society, 41:113–128, 1979.

E. S. Blake, C. W. Landsea, and E. J. Gibney. The deadliest, costliest,

and most intense United States tropical cyclones from 1851 to 2010 (and

other frequently requested hurricane facts). Technical Report Technical

Memorandum NWS NHC-6, NOAA, National Weather Service, National

Hurricane Center, Miami, Florida, August 2011.

L. Bovens and W. Rabinowicz. Democratic answers to complex

questions — an epistemic perspective. Synthese, 150:131–153, 2006.

G. E. P. Box and G. C. Tiao. Bayesian Inference in Statistical Analysis.

Addison-Wesley, Reading, Massachusetts, 1973.

T. W. Cannon. Light and radiation. In C. DeCusatis, editor, Handbookof Applied Photometry, chapter 1, pages 1–32. Springer Verlag, New York,

New York, 1998.

R. Carnap. Logical Foundations of Probability. University of Chicago

Press, Chicago, Illinois, 2nd edition, 1962.

G. Casella and R. L. Berger. Statistical Inference. Duxbury, Pacific

Grove, California, 2nd edition, 2002.

N. Clee. Who’s the daddy of them all? In Observer Sport Monthly.

Guardian News and Media Limited, Manchester, UK, Sunday March 4,

2007.

R. T. Clemen and R. L. Winkler. Combining probability distributions

from experts in risk analysis. Risk Analysis, 19:187–203, 1999.

R. T. Cox. Probability, frequency and reasonable expectation. AmericanJournal of Physics, 14:1–13, 1946.

R. T. Cox. The Algebra of Probable Inference. The Johns Hopkins Press,

Baltimore, Maryland, 1961.

A. C. Davison and D. Hinkley. Bootstrap Methods and theirApplications. Cambridge University Press, New York, NY, 1997.

B. de Finetti. La prévision: ses lois logiques, ses sources subjectives.

Anales de l’Institut Henri Poincaré, 7:1–68, 1937.

B. de Finetti. Theory of Probability: A critical introductory treatment.

John Wiley & Sons, Chichester, 1990. Two volumes, translated from the